Connected TVs now own the top spot for digital video ad impressions. The total share in Q4 2018 matched the combined share of desktop/laptop and mobile. Ad based offerings from Roku, Hulu and YouTube are growing rapidly with no end in sight. Companies like The Trade Desk are calling connected TV growth the fastest growing market they have seen and we will ever see in marketing. This market is predominatly programmatic and highly efficient and begging for every marketer to pay attention.

May Sales & Tariffs

Census Bureau released the May retail sales figures on Friday. The report was particularly strong considering all the chatter of tariffs potentially slowing retail sales as price increases trickle down to consumers. April was revised upward from the initial report which drove the GDP estimates higher for many analysts.

The overall number for May was +3.2% from 2018 with winners being nonstore (online) posting the routine >10% increase, food services/restaurants, health and auto retailers. Those in the negative year over year were sporting goods, clothing, electronics/appliances and department stores.

Interestingly, the April number for electronics/appliances figure was positive in April but negative in May. Bespoke highlighted how the share of imports of steel and aluminum has already shifting away from China to Mexico and Vietnam to avoid the tariffs (see below). It may be too early to see the true impact of higher prices passed onto the consumer but this and jobs report were suprisingly strong.

Confusing Ecommerce Delivery Options

The ongoing battle between the three major retailers has me completely confused and befuddled. Let’s just look at the options by retailer:

Amazon

Prime - Guaranteed 2 day shipping comes with an annual or monthly subscription for the large marjoity of what they offer on the site.

Prime Pantry - An extra $4.99 per month for unlimited deliveries over $10, free for Prime members with orders over $35.

Prime Fresh - Strictly for groceries.

Subscribe & Save - Subscription on items delivered each month (or every few months) where savings increases with the more you add.

Add-On - Can only be added to orders over $25.

Prime Now (Amazon) - $4.99 per delivery in a few hours unless over $35.

Prime Now (Whole Foods) - $4.99 per delivery for Whole Foods items (some products overlap with Amazon catalog) unless over $35.

Target

Restock - Next day delivery for $2.99 unless over $35.

Shipt (just announced) - Same day delivery for $9.99.

Subscription - Delivered each month.

2-day Ship - Free over $35.

Pick-Up In Store - No fee.

Drive Up - No fee.

Google Express - Free over $15.

Walmart

2-day Ship - Free over $35.

Pick-Up In Store - No fee.

Drive Up - No Fee.

Unlimited Grocery Delivery - New subscription service for $99 annual fee.

I likely missed several options but is anyone confused yet? Amazon is the most confusing and the Whole Foods acquisition surely hasn’t helped. Although the array of options likely hasn’t slowed the transition to ecommerce and led to more consumer options, the experience of selecting which and understanding your options is incredibly cumbersome.

Food Delivery Wars

Amazon surprised quite a few people yesterday by announcing they are shutting down their restaurant delivery service in the US later this month. Similar to the shutdown in London last November and subsequent investment in Deliveroo, many believe Amazon will invest in one of the other food delivery providers in their next round.

With recently public competition like Uber, heavily funded private companies like Postmates and DoorDash and niche players like Square’s Caviar, there is no shortage of competition. Just ask the largest incumbent Grubhub who owns Seamless:

Although it is projected by William Blair that restaurant deliveries will only account 11% of total restaurant by 2022, the space is growing RAPIDLY and all that growth is coming from the delivery providers:

So with Amazon out of the race, what happens next? I would assume either Postmates or DoorDash is acquired by Uber to bolster their Uber Eats offering. In my opinion, Grubhub just doesn’t have the confidence of their shareholder base, the cash or ability to add a secondary offering of stock to buy either. I believe Square truly isn’t interested in this business and has positioned Caviar as the higher end offering. Jack Dorsey wakes up each morning to be a payments and social media guy, not the delivery king. Regardless, this is a scale game and you have some hungry competitors who are likely looking to consolidate the market into more of a duopoly to gain further leverage:

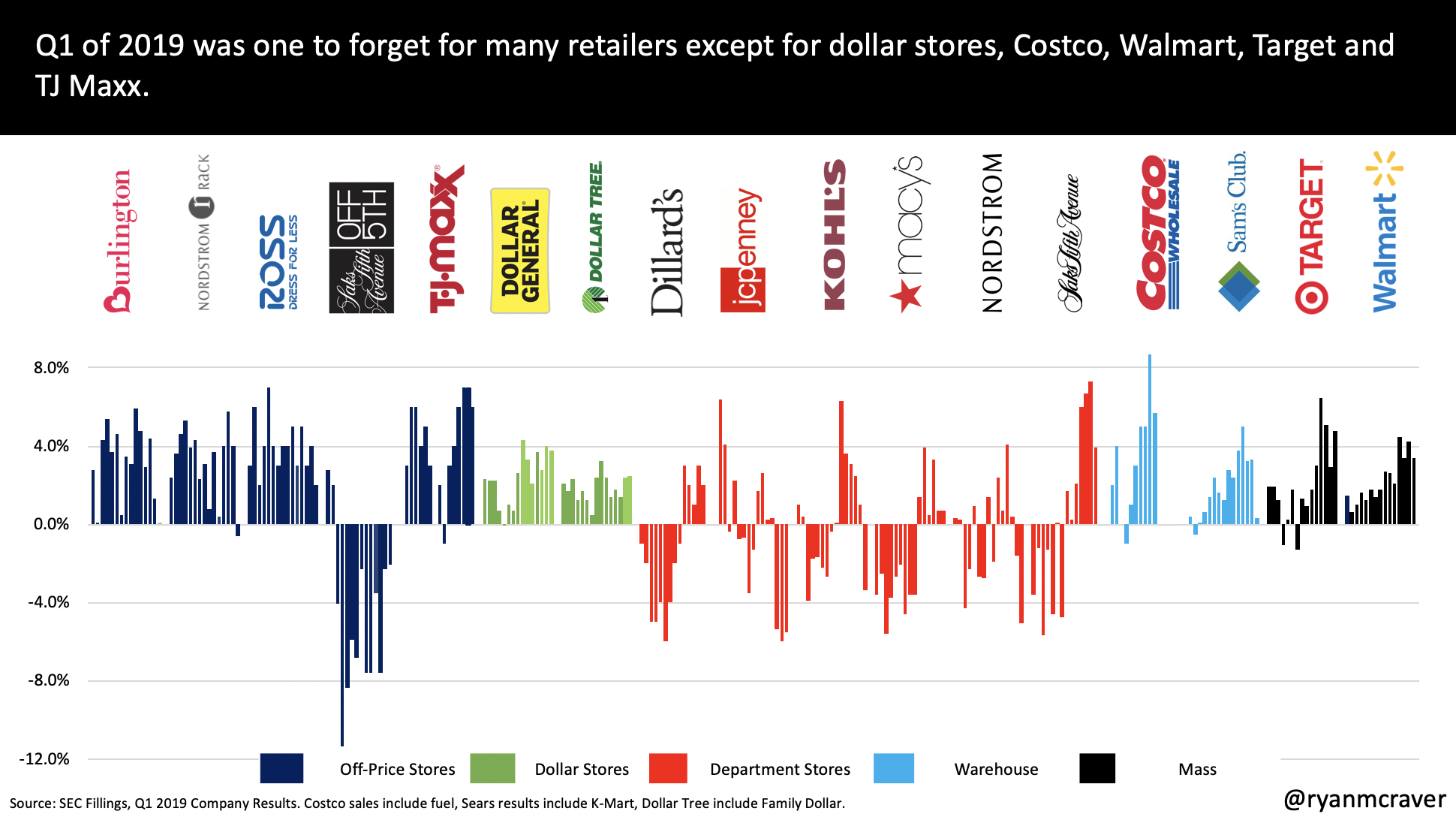

A Quarter to Forget For Many Retailers

Last night concluded the Q1 earnings season for a majority of the key retailers. For many of those retailers, Q1 was one to forget. Some of the data points I was left with:

Nordstrom Full Line and Nordstrom Rack posted the worst negative comps since the depression at -5.1% and -0.6% respectively.

Kohls surprised many with a -3.4% comp (first negative since Q2 2017) and now saying there will be negative earnings growth for the full year.

Ross and Burlington posted slowing comps versus previous quarters.

With all of that said, there was some positive news:

Costco remains on fire posting the 5th consecutive month of >7.0% comp in the US.

Walmart and Target both posted respectable increases of 3.4% and 4.8% respectively.

TJ Maxx remains hot with 4th consecutive quarter of >6.0% comp.

Dollar Stores continue to gain share with 2.5-4.0% comp increases.

The trends continue. Department Stores losing share to the mass, off price and dollar stores continues with the data showing there is no slowing to the shift.

Roku Momentum Continues

Roku recently released their earnings with strong year over year streaming and continued growth of ARPU and users. Most growth rates were slightly higher than Q4. Some of the highlights for Q1:

Platform revenue grew 78% year over year (up slightly from 77% last quarter) for the quarter to $134mm.

Streaming hours grew close to 74% year over year (up slightly from 70% last quarter) for the quarter to 8.9 billion hours.

The average revenue per user is now just under $18 with over 27 million active users (40% growth rate year over year for the quarter).

Most impressively, Roku now estimates their software is on 1 in 3 smart TVs sold in the US, this is up from 1 in 4 in previous quarters. Roku is now the #1 smart TV OS.

Other than a slightly slower increase to ARPU, this was a continued vote of confidence for Roku playing a leading role in the switch to on demand streaming.

Amazon 1 Day Shipping Since 2017

Amazon made quite a few waves about one day delivery. It’s been something Amazon has been capable of for nearly two years. Here is the evolution leading up to 48 states being within 1 day of delivery in 2017.

Amazon = The Service Provider

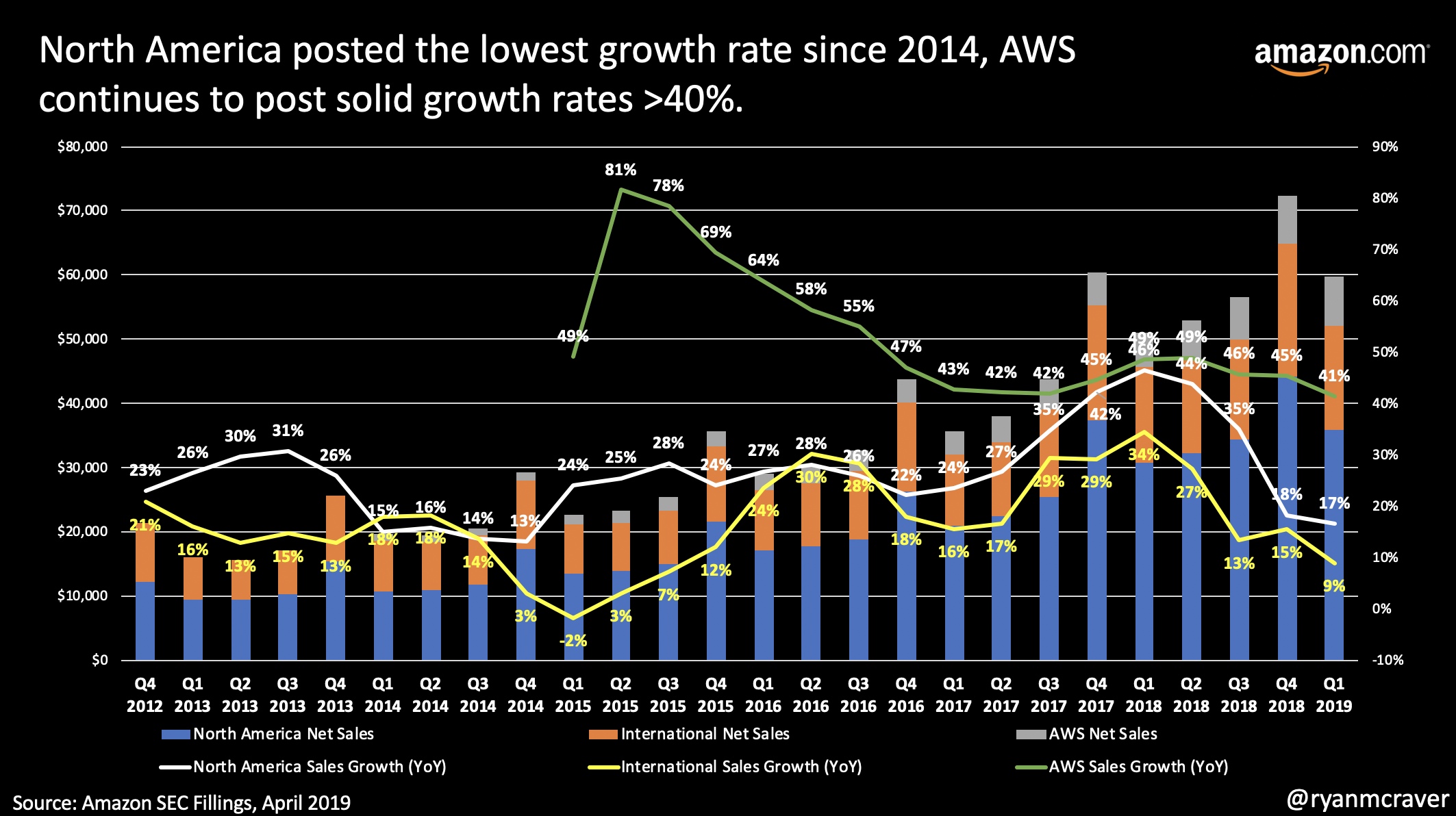

This was a well played and planned earnings release by Amazon. The January earnings release saw the slowest sales growth rate in 16 quarters which continued to slow even further in the recently quarter. The North America business hadn’t posted this small of an increase since 2014 and international since 2015. Whether due to the law of large numbers or the competition stepping up their game, one thing is certain. Amazon is becoming much more profitable as the company becomes less reliant on online owned sales.

So why was Amazon trading up post earnings? In the latest quarter, online accounted for less than 50% of the total revenue in the quarter. Third party revenue (seller services) accounted for 18% with the real growth coming from AWS and subscriptions at 13% (up from 10%) and 7% respectively (up from 5%). Services, services, services = profits, profits, profits. Yes, the p word that no one believes Amazon was capable of just 2 short years ago.

Despite some of the weakest revenue growth figures in years, Wall Street and Main Street still like what they heard and still believe in the Prime, AWS, Services shift.

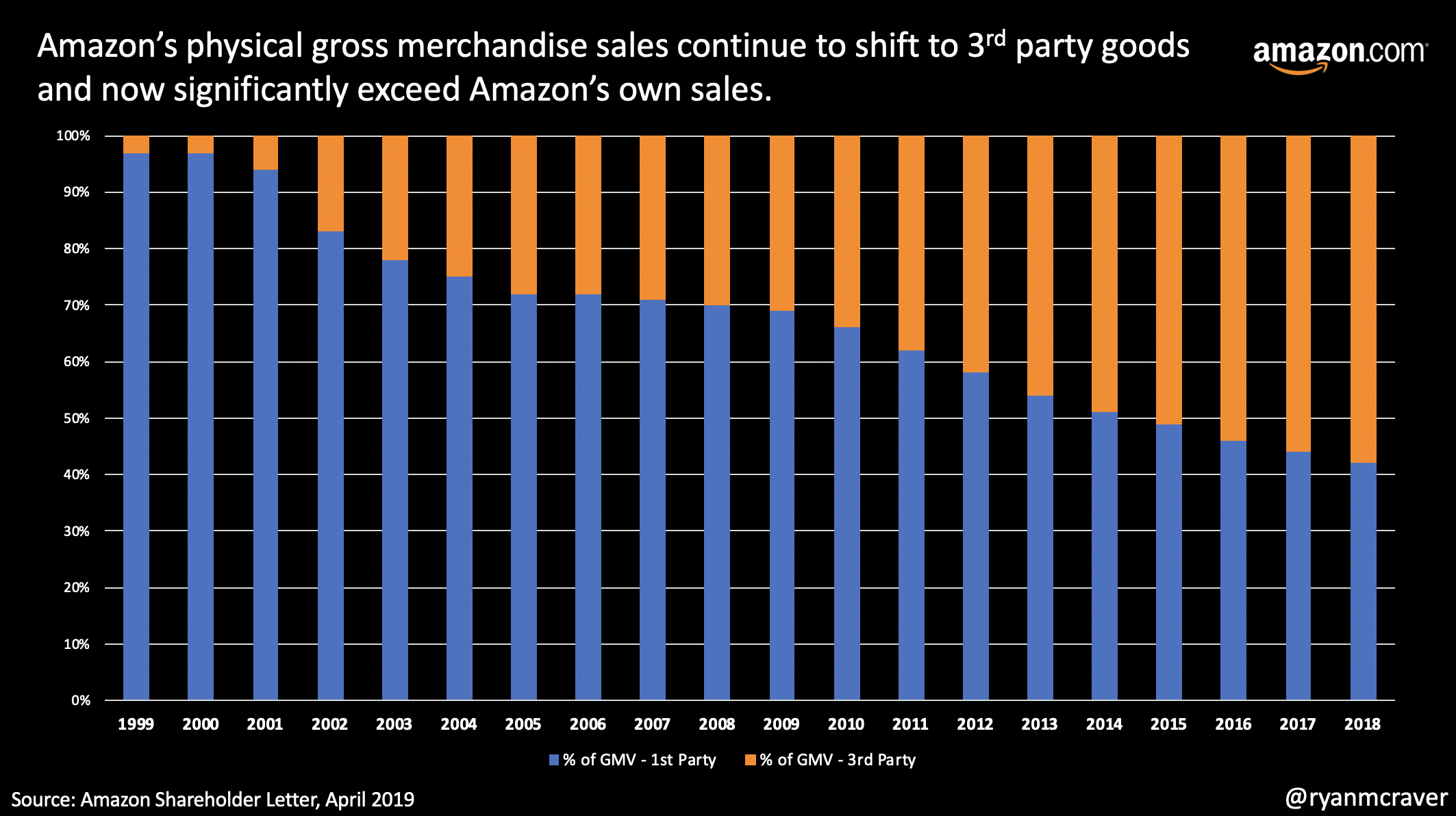

Amazon's Quest to Become eBay and Alibaba

If anyone had any doubt that Amazon is sick of owning inventory and is more focused on selling services than Apple is, look no further than Jeff Bezos comments in today’s shareholder letter:

The percentages represent the share of physical gross merchandise sales sold on Amazon by independent third party sellers – mostly small- and medium-sized businesses – as opposed to Amazon retail’s own first party sales. Third-party sales have grown from 3% of the total to 58%. To put it bluntly: Third-party sellers are kicking our first party butt. Badly. And it’s a high bar too because our first-party business has grown dramatically over that period, from $1.6 billion in 1999 to $117 billion this past year. The compound annual growth rate for our first-party business in that time period is 25%. But in that same time, third-party sales have grown from $0.1 billion to $160 billion – a compound annual growth rate of 52%. To provide an external benchmark, eBay’s gross merchandise sales in that period have grown at a compound rate of 20%, from $2.8 billion to $95 billion. Why did independent sellers do so much better selling on Amazon than they did on eBay?

Although Jeff takes a swing at eBay, Amazon truly realizes the beauty of the inventory-less business models used by eBay and Alibaba. Lower cash requirements and better margins. When you chart out the growth, the growth is truly staggering:

Online Dating Monopoly

Mind boggling how cornered this market is by MatchGroup (tinder, PlentyofFish, match.com, okcupid), as online became the most popular way to meet:

Scooter Stats

Fascinating statistics and reporting on the economics of scooters from players like Lime and Bird. Not looking like the best of business models.

The average lifespan of a scooter was 28.8 days

The median lifespan was 26 days

The average vehicle went 163.2 miles over 92 trips during its lifetime

Five of the 129 initial-cohort scooters disappeared the same day they went into service (a lifespan of “0” days)

The scooter with the longest lifespan made it 112 days, last appearing in the data on Nov. 29

Only seven of 129 scooters lasted more than 60 days

Utilization

The average trip lasted 18 minutes

The average scooter did 3.49 rides per day

Revenue

Bird charges $1 to unlock a scooter and $0.15 per minute

At 18 minutes, the average trip generated $3.70 in revenue (note that this, based on three months of data in Louisville, is nearly identical to the $3.65 in revenue per ride Bird reportedly told investors it was averaging as of June)

At 3.49 rides per day, the average scooter generated $12.91 in revenue per day

General costs, based on reporting by The Information

Bird spent $1.72 per ride on charging costs

It spent another $0.51 per ride, on average, on repairs

Credit-card fees cost $0.41 per ride

Customer support adds $0.06 per ride

Insurance is $0.05 per ride

This adds up to $2.75 in what you could consider operating costs per ride

Louisville-specific costs, from the city’s dockless vehicle policy

A company pays $2,000 for a probationary license (required for the first six months of operation)

It pays an additional $1,000 to receive a full operating license

The city charges an annual $50 fee per allotted dockless vehicle

Plus a daily $1 fee per dockless vehicle

And $100 per designated group parking area

Louisville scooternomics, in sum:

A scooter generates $3.70 in revenue per ride

Deducting per-ride costs of charging, repairs, credit-card fees, customer support, and insurance, leaves $0.95 per ride

Multiplied by 3.49 rides per day is $3.32 in net revenue per scooter per day

Minus the city’s $1 daily fee leaves $2.32

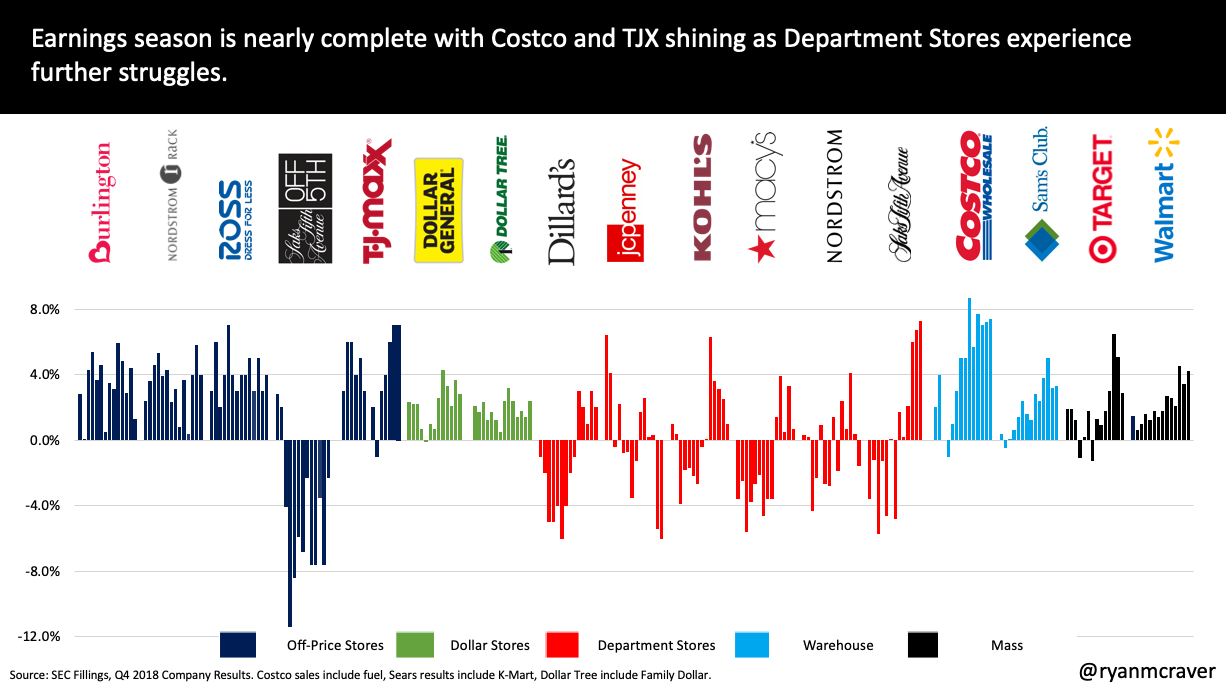

Retail Share Shifts Starting 2019: Costco & TJX

Comp sales released during earnings are a backward indicator of success in the preceding quarter but generally provide a view of how market share is shifting amongst like for like retailers as well as share leaving one sector to another. A couple of takeaways from this past quarter:

Costco is on fire. The warehouse club has posted 4 consecutive quarters of >7.0%. Phenomenal.

Off-price remains positive. All majors such as Burlington, Nordstrom Rack, Ross and TJX posted increases. Burlington was weakest amongst the majors and TJX posted a 3rd straight result >6.0%.

Big box mass sees above average results with Walmart posting an impressive 4.2% and Target just under 3.0%.

Department Stores remain difficult. From the abysmal results of JC Penney to the tepid results of Macy’s and Kohls.

I remain convinced that Costco still remains the best play in retail with their strong membership base moat and industry leading comp results. Second to Costco is TJX as they gain share from Department Stores and other retail bankruptcies.

Managing Email

Managing email and the pursuit of Inbox Zero is a daily battle. For some unknown reason, I am determined to always seek ways to make managing email more effective and efficient. Whether on Office 365, Google Apps or another mail provider, each of today’s apps have different functionality and use cases and none of them are perfect. Here are the latest apps I am using by device:

iPad/iPhone

Outlook - By far the best app I know of on iPad for email and provides. This has been my go-to since the days of Accompli (Microsoft acquired). Gmail doesn’t provide the individual email deletes in thread and really bugs me when filing that you can’t type in which folder in place of scrolling.

Laptop/Desktop (Browser or App)

Superhuman - Gmail on steroids. Keyboard shortcuts are more intuitive and wide ranging so you literally never touch the mouse. Search is faster, everything based in Chrome in place of another program and definitely the closest I have come to Inbox Zero. Three downsides: only available for Gmail/Google, partial calendar integration and iPhone app is quite slow.

What have I tried? Mail, Newton, Airmail, Gmail, Outlook Web, you name it. None are perfect but Outlook continues to hang and Superhuman is definitely onto something.

Roku Advertising Powers Higher

Roku recently released their earning and their results are quite impressive as they shift into an advertising platform built on TVs and through streaming sticks. Some of the highlights for Q4:

Platform revenue grew 77% year over year for the quarter to $151mm, a total of $416mm for the full year.

Streaming hours grew close to 70% year over year for the quarter to 7.3 billion hours.

The average revenue per user is now just under $18 with over 27 million active users (40% growth rate year over year for the quarter).

The idea of more targeted advertising to consumers that are paying better attention as cords continue to be cut continues to shine. Roku seems poised to benefit for the foreseeable future.

Ecommerce Needs Competition

eMarketer outlined where they believe the 2019 e-commerce market share will fall by end of year. The major gainer is expected to be Walmart with a growth of nearly 33% to $27.81 billion or 4.6% share (earlier today they announced a year over year growth of 40%). Even with that impressive number, there is no comparison to Amazon who is projected to grow 20% to $282.52 billion or an astounding 47.0% share. EBay meanwhile is number 2 with 6.1% market share but not truly growing.

Just look at the cliff in this bar chart to highlight the top 10 by market share. This continues each year and the gap only grows as the overall market grows faster and Amazon maintains its’ considerable lead.

Retail Online Sales Share (2019 via eMarketer)

I believe it is in the best interest of the e-commerce market to have at least two majors facing head to head followed by a long tail. That would at minium make this ecommerce race an oligopoly which not ideal but would be an improvement. With the current magnitude of separation continuing year over year and growing, I have become convinced the market needs a massive consolidation of market share to see a true competition and overall market health.

Given the list of retailers, there are a couple of options for tie-ups:

Walmart buying eBay - Extends their marketplace model with no further inventory needs.

Walmart buying Quarate (QVC, HSN, Zulily) - TV platform extension along with stable of brands to extend into stores and digital channels.

Walmart buying Wayfair - Fast growing home goods retailer with growing stable of sellers and advertising revenue.

Beyond the three tie-ups above, no other scenarios provide a meaningful increase in market share or are unlikely. Apple wouldn’t tie up with other retailers and I can’t imagine Costco growing outside their warehouse comfort zone. What say you?

Note: An eBay or Walmart could potentially acquire a platform provider like Farfetch or Shopify to roll up the market share of several brands but the general idea here would be roll up individual .coms or a handful of .coms.

Retail.coms Selling Ads

The sting of driving traffic to retailer .com sites through advertising via the Facebook and Google duopoly is expensive. The cost of shipping orders in the age of “free shipping” is even more expensive. So how else can retailers drive a higher revenue per visitor? Ads.

Each retailer knows the value of their traffic and understands the value of either selling the promotion of products on their site or linking out to other sites. Each retailer is taking one of two approaches: 1) self help advertising tools allowing any brand or seller to purchase keywords using budgets; 2) middle man large agencies providing limited access to keywords using budgets.

Amazon realized the value of ads early and built an extensive platform for brands to self administer their ads similar to Google. That business which is part of the “Other” category drove over $3b in revenue in Q4 2018.

Wayfair recently released their platform allowing brands and sellers to self administer their ads. Watch as the Wayfair narrative shifts from owned sales to services revenue (marketplace, advertising, etc.)

Whilst Amazon and Wayfair are focused on allowing anyone to gain access to spend on marketing, Walmart (who currently earning the most traffic of any retailer in the US) still sells the majority of their ads via large agencies such as Criteo. This is surprising as Walmart is focused on becoming more of a marketplace for small and medium size businesses yet is so restrictive on new accounts and access to marketing.

Traditional retailers that do not employ the marketplace model such Kohls, Target and Macys are even more guarded. These retailers ONLY allow marketing via large agencies and to those brands who sell them directly.

As this space continues to evolve, we will see more and more ads as brands realize there are very few sales earned via organic searches and retailers understand the value of captive customers and what a brand is willing to pay for a click.

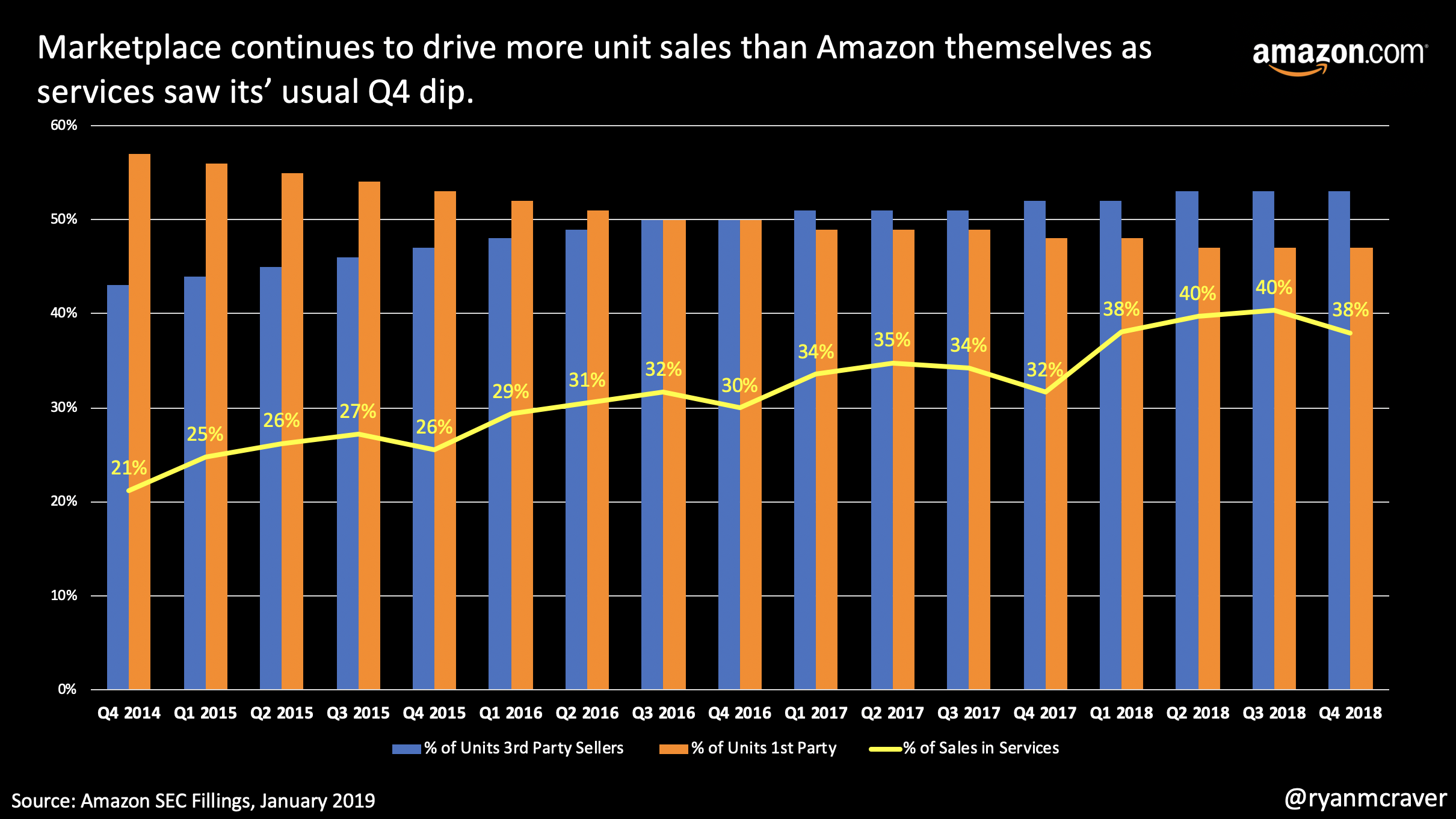

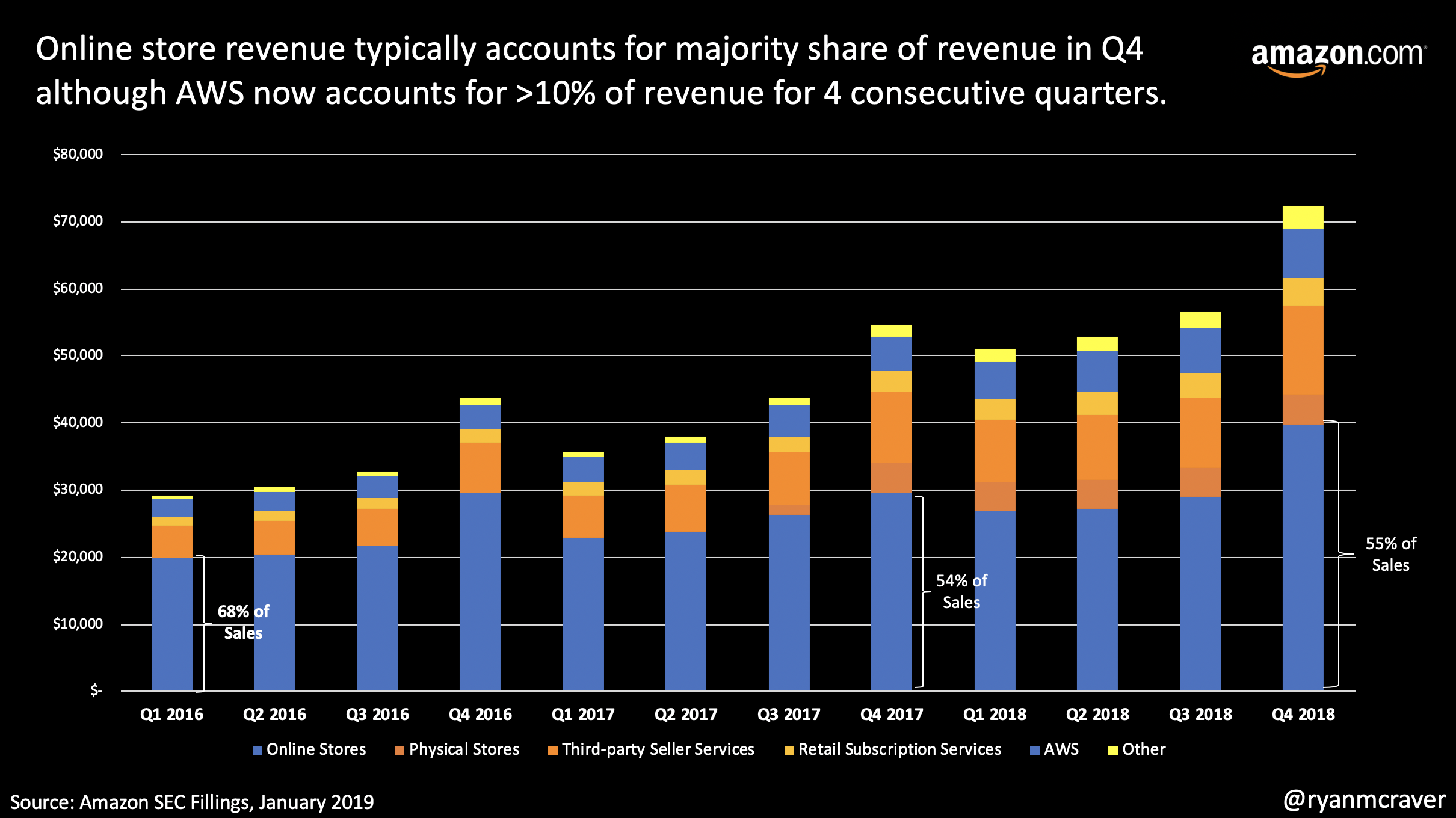

Amazon Earnings Hot Take

As the Amazon earnings hit the news wire, the stock initially traded up after hours but after sifting through the nearly 20 pages, the forecast drove the stock lower. A few takeaways from the latest earnings release:

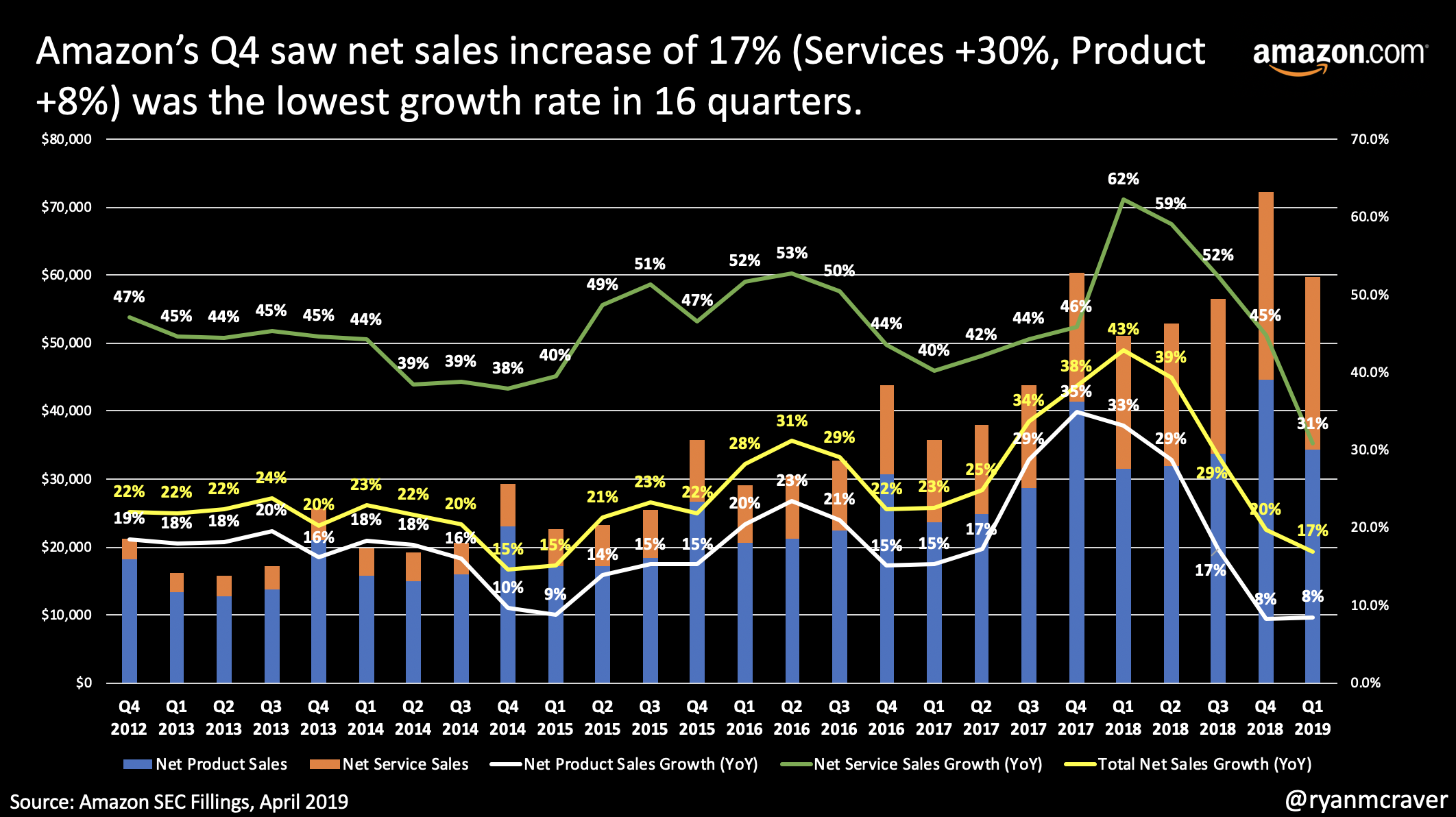

The overall revenue grew just under 20% which is a low for a number of years.

Q4 typically sees the lowest growth rates given the large base of retail sales in Q4 in North America.

North America sales saw one of weakest quarters in recent years. I believe this is likely due to Amazon adding in long term storage fees for 3rd party sellers that led to sellers pulling inventory and thus impacting sales. Amazon has since retracted those long term storage fees beginning February 15.

The International revenue was up 15% which is a slight uptick from the 13% posted last quarter. Given recent Indian restrictions being announced, the Q1 forecast is a bit cloudy.

The most profitable businesses continue to have the highest growth rates. AWS has now accounted for >10% of the revenue for the 4th consecutive quarter. The “Other” category that includes Advertising grew 90%+ year over year.

3rd party sales via the marketplace continue to gain share year over year as Amazon pullsback on 1st party owned sales.

Whole Foods/store sales saw a decline as the company calendarized their results and highlighted that any sales driven by Amazon and delivered fall into the online sales bucket.

Bottom line: Whilst the revenue growth numbers were disappointing, Amazon’s key offerings (AWS, Services and Other) continue to grow rapidly and are bringing much desired profitability.

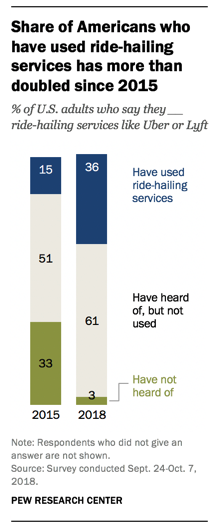

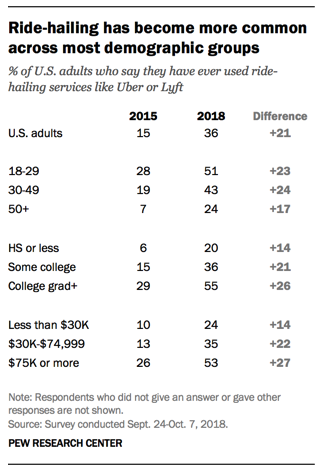

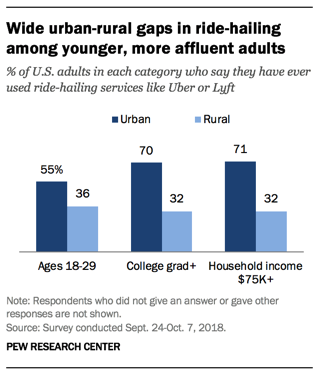

Ride-Hailing App Stats

Pew recently outlined the dramatic rise of ride-hailing services such as Uber, Lyft, Juno, etc. There were a few stats that stuck out to me:

Only 3% of respondents hadn’t heard of ride-hailing services, this is down from 33% in 2015

36% of respondents have used ride-hailing, this is up from 15% in 2015

Within urban environments, >70% of college grads and high income households have used ride-hailing

The report doesn’t outline frequency of use but still impressive that awareness is nearly saturated across rural and urban locations and all age groups. Take a look at the full report screenshots below.

India Marketplace Smackdown

India recently launched legislation that has brought quite a bit of confusion but is clearly a setback for Amazon and Walmart (Flipkart stake):

“An entity having equity participation by e-commerce marketplace entity or its group companies, or having control on its inventory by e-commerce marketplace entity or its group companies, will not be permitted to sell its products on the platform run by such marketplace entity,” the commerce ministry said in a statement.

E-commerce companies can make bulk purchases through their wholesale units or other group companies that in turn sell the products to select sellers, such as their affiliates or other companies with which they have agreements.

The ruling implies that marketplaces such as Amazon and Flipkart will not be able to offer their own private label products or exclusive products on their respective platforms. All vendors will have to be provided the same terms and no vendor can be forced to exclusivity. I would assume Amazon and Flipkart will contest the ruling before the February 1, 2019 enforcement date.

Reading Into Amazon Seller Fee Changes

As often pointed out, greater than 50% of the product sold on Amazon is sold by small and medium size businesses around the world. In fact, it is estimated that more than 2 million sellers on the US marketplace are selling more than >$1 million in retail sales annually. These sellers use Amazon’s customers/traffic, logistics network and marketing capabilities to sell their product on Amazon each and every day. This type of business is incredibly lucrative for Amazon as they never take ownership of inventory.

Just yesterday Amazon made some changes to those fees charged to sellers that typically provide a viewpoint on the type of product Amazon is looking to attract or how their current businesses are performing. Here are my thoughts:

Storage Fees - Amazon surprised most sellers by eliminating the 6-12 month long term storage charges. This goes against their recent increase and monthly long term storage charge that began to charge monthly in Summer 2018. This leads me to believe that Amazon saw significant drops in inventory held by sellers that led to higher out of stocks and missed sales.

Referral Fees - Three years ago Amazon led everyone to believe they cared most about Apparel. In reality that was a massive head fake as Amazon eventually realized that everyone’s wallet is spent on grocery, health and beauty. You can see that is evident in Amazon dropping the referral fees in both categories. Additionally, they are dropping the referral fees in Jewelry for items over $250. This tells me they are trying to recruit less trinkets and trash and more high end jewelry.

Fulfillment Fees - Generally there were very little changes. Amazon did however simplify the Subscribe & Save fee structure showing their desire to build this business further.

Bottom line: All the above changes highlight Amazon doubling down on key categories like Grocery and Health along with an understanding that Sellers drive the overall marketplace with their consigned inventory.