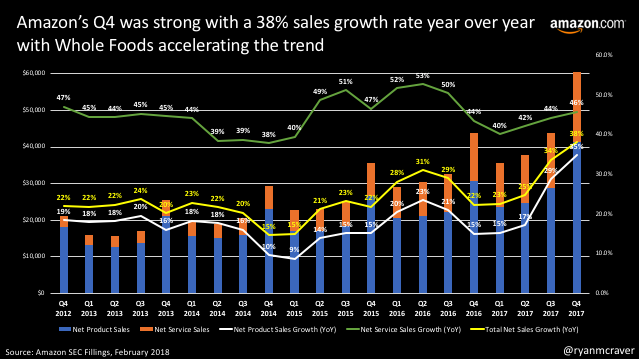

Another quarter with monstrous growth of which most was expected due to the Whole Foods acquisition. A few major themes:

- Growth Accelerates: Top line revenue growth was 38% of which Services and Product Sales grew 35% and 46% respectively.

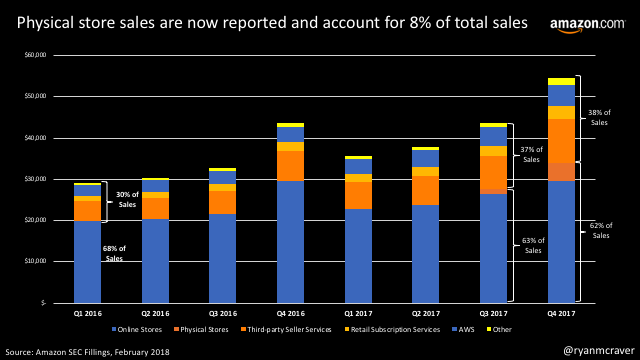

- The Shift is On: The shift to brick and mortar continues as stores now account for 8% of sales and online accounts for 54%, down from 68% last year.

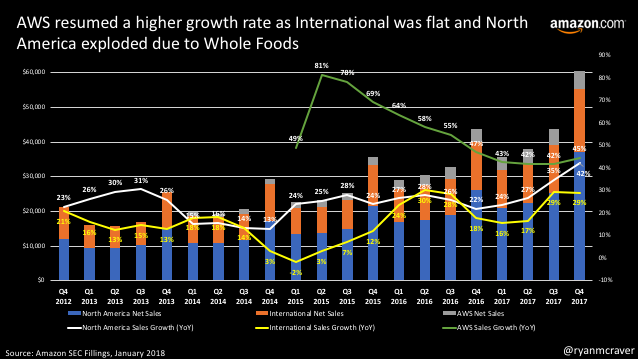

- Services, Services, Services: Growth including AWS was phenomenal...and profitable.

Nothing to worry about here. However, as the effects of the Whole Foods growth disapears after 2 more quarters, international will need to ramp further to maintain the 30%+ growth rates investors are accustomed to. Updated charts below.